A Beginner’s Guide to Reverse 1031 Exchanges

A reverse exchange can be very useful to real estate investors when you have an investment opportunity that can't wait, but you don't have a buyer for your current property.

By using the reverse exchange, you can secure the new property and still sell your old investment property in a 1031 exchange that defers your taxes.

Let’s look at how these transactions work and how they can benefit you.

Reverse 1031 Exchange Rules

A taxpayer sells the old property (the “relinquished property”) before acquiring the new property (the “replacement property") under IRS rules for a traditional 1031 exchange.

Due to various circumstances, however, a taxpayer may be faced with losing the opportunity to acquire their ideal replacement property. The investor might not have found a buyer for their relinquished property, or that property may not even be listed for sale yet. Even if the relinquished property is already under contract, the closing date may not be before the investor would purchase the replacement property.

In these situations, an investor can use a reverse 1031 exchange to facilitate the real estate transaction.

What Is a Reverse Exchange?

A traditional replacement parked reverse exchange is a 1031 transaction where the closing date of the replacement property occurs before the closing date for the sale of the relinquished property. Ironically, the way you do a reverse exchange is to organize the transaction, so it appears to be in the proper order.

The IRS created a set of rules providing a “safe harbor” for reverse exchanges in 2000, which means the IRS recognizes the structure and won’t challenge these transactions, as they are preapproved.

How Does a Reverse Exchange Work?

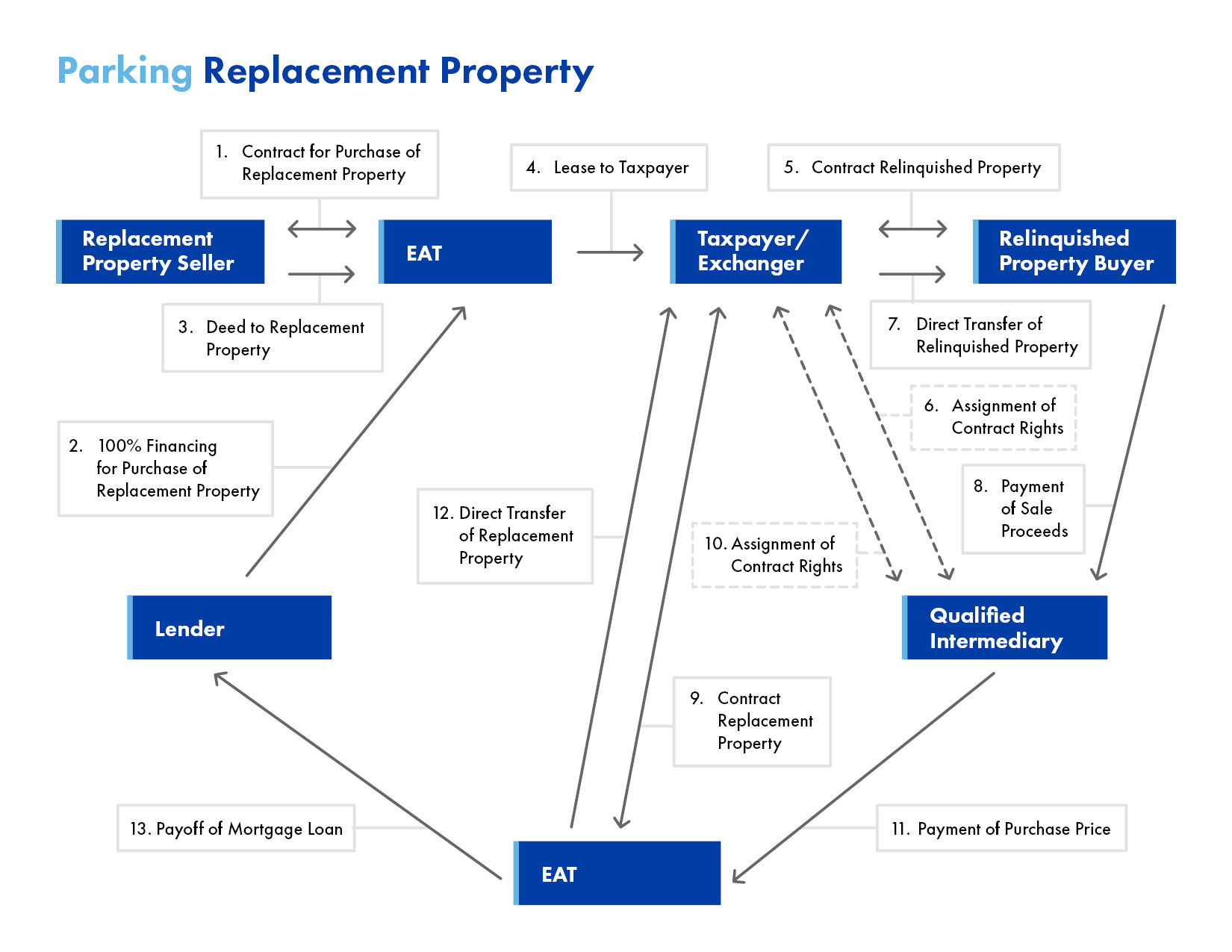

According to the rules, a taxpayer can hire an exchange company to work as a Qualified Intermediary. The Qualified Intermediary will create an entity known in the regulations as an Exchange Accommodation Titleholder (EAT).

The EAT, through the Qualified Intermediary, acquires the replacement property and holds it on the taxpayer’s behalf. From there, a taxpayer has up to 180 days to sell the relinquished property and finish the exchange for the replacement property that the EAT is holding.

As as result, the taxpayer doesn’t fully acquire the replacement property before the sale of the relinquished property, so the 1031 exchange can be done in the proper sequence. For more information, view our reverse 1031 exchange diagram for a complete look at how the process works.

{kind=link}

Financing in a Reverse Exchange

It’s important to understand how to finance a reverse 1031 exchange. The Qualified Intermediary doesn’t provide funds for the purchase. Instead, the money comes from a loan from the taxpayer to the Qualified Intermediary or through a bank loan. The loan is paid off once the relinquished property is sold and the money becomes available.

During the period where the replacement property is held by the Qualified Intermediary, it leases the property to the taxpayer, which allows the investor to sublease the property to tenants and collect and retain the rent. The taxpayer is responsible for expenses associated with the property as part of the lease.

At the end of the transaction, the Qualified Intermediary simply makes it fee, and all the profits and costs of the new property are retained by the investor.

Cost of a Reverse Exchange

The cost of a reverse 1031 exchange varies based on multiple factors. For example, the type of property (multifamily, retail, industrial, etc.), the value of the property, how long the EAT will be on title and the type of financing or lending source can all impact the cost.

The Qualified Intermediary holds the title to the new property temporarily, but the costs associated with the buildings, maintenance, and more are passed on to the end buyer.

Also, the fee the Qualified Intermediary charges to act as the Exchange Accommodation Titleholder must be factored into the cost of the transaction.

Relationship Between a Reverse Exchange and a Forward Exchange

Investors may be confused about the relationship between a reverse exchange and the regular 1031 forward exchange. “Why do I need a regular exchange since I’m doing (and paying for) a reverse exchange?” they may ask.

The reason is that even though this is all one transaction, there are multiple steps in the process. The reverse exchange is done to ensure you have access to the replacement property rather than losing it to another buyer. Then, once you sell the relinquished property, you execute a regular 1031 exchange to officially replace it with the replacement property.

That means you’re working with two entities: an Exchange Accommodation Titleholder to hold the new property while you sell the old one, and a Qualified Intermediary (QI) to allow you to replace the old property with the new one.

Case Study: An Example of a Reverse 1031 Exchange

Providing an example of a reverse 1031 exchange can help make it easier to understand.

A physician, Mr. Black, wanted to do a 1031 exchange, but he needed to purchase the replacement property right away, or he would miss out on the opportunity. However, Mr. Black did not have a buyer in place for the property he planned to relinquish.

Because Mr. Black cannot own both the relinquished property and the replacement property and exchange with himself, he must hire the services of a Qualified Intermediary (QI) and perform a Reverse Exchange. This structure will allow Mr. Black to park title of the replacement property with the QI while he finds a buyer for his relinquished property. The entity used to park title is known as the EAT – Exchange Accommodation Titleholder.

Mr. Black got a bank loan to buy the property, and the loan was made to the EAT, a newly formed LLC where the Qualified Intermediary was the only member. The loan was secured by a mortgage on the new property, and once the new property was obtained and the title was transferred to the Exchange Accommodation Titleholder – EAT, Mr. Black had 180 days to sell the old property and execute a 1031 exchange.

Mr. Black was able to sell the relinquished property five months later and the equity from that sale was deposited into the regular 1031 exchange account. Then, Mr. Black told the QI he had identified and appointed to transfer the money to the Qualified Intermediary to pay down part of the loan on the new property.

Finally, Mr. Black took possession of the new property through a regular 1031 exchange and was responsible for paying back the remaining loan through the new property’s mortgage.

As you can see, the reverse exchange can be a valuable tool for investors who need to move quickly to take advantage of an excellent investment opportunity. As long as the taxpayer can sell the original property within 180 days, they can still swap investments through a 1031 exchange and defer the associated taxes.

Read More

Insights

Research to help you make knowledgeable investment decisions